Both US-based companies and those headquartered in othercountries produce the same primary financial statements—IncomeStatement, Balance Sheet, and Statement of Cash Flows. Concepts Statements give the Financial Accounting StandardsBoard (FASB) a guide to creating accounting principles and considerthe limitations of financial statement reporting. These examples will show you how to adjust an unadjusted trial balance looks like.

IFRS Connection

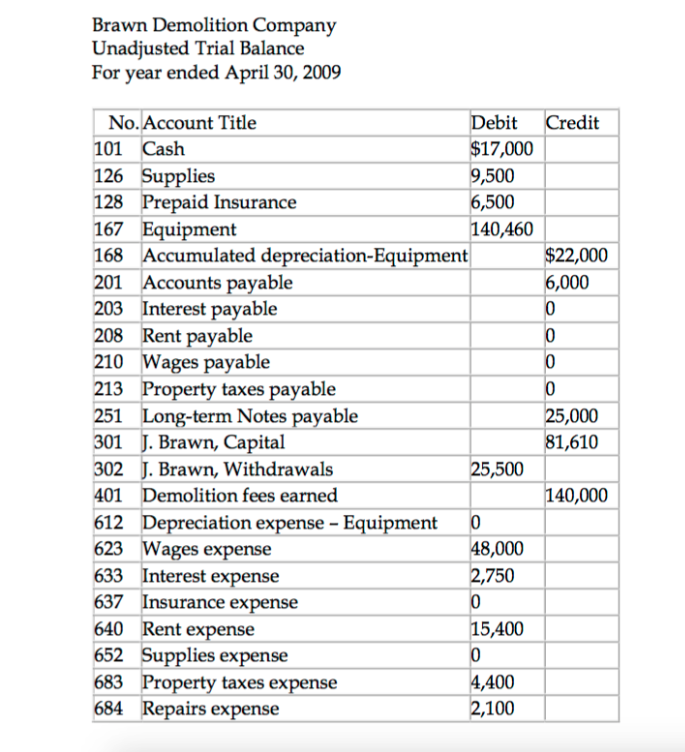

You have beentasked with determining if this transition is appropriate. The salon had previously used cash basis accounting to prepare its financial records but now considers switching to an accrual basis method. You have been tasked with determining if this transition is appropriate. Hence, the trial balance includes all considerable adjustments, which is termed as adjustment trial balance. There are instances when companies end up missing out mentioning the transactions that have occurred in the bookkeeping records.

Income Statement and Balance Sheet

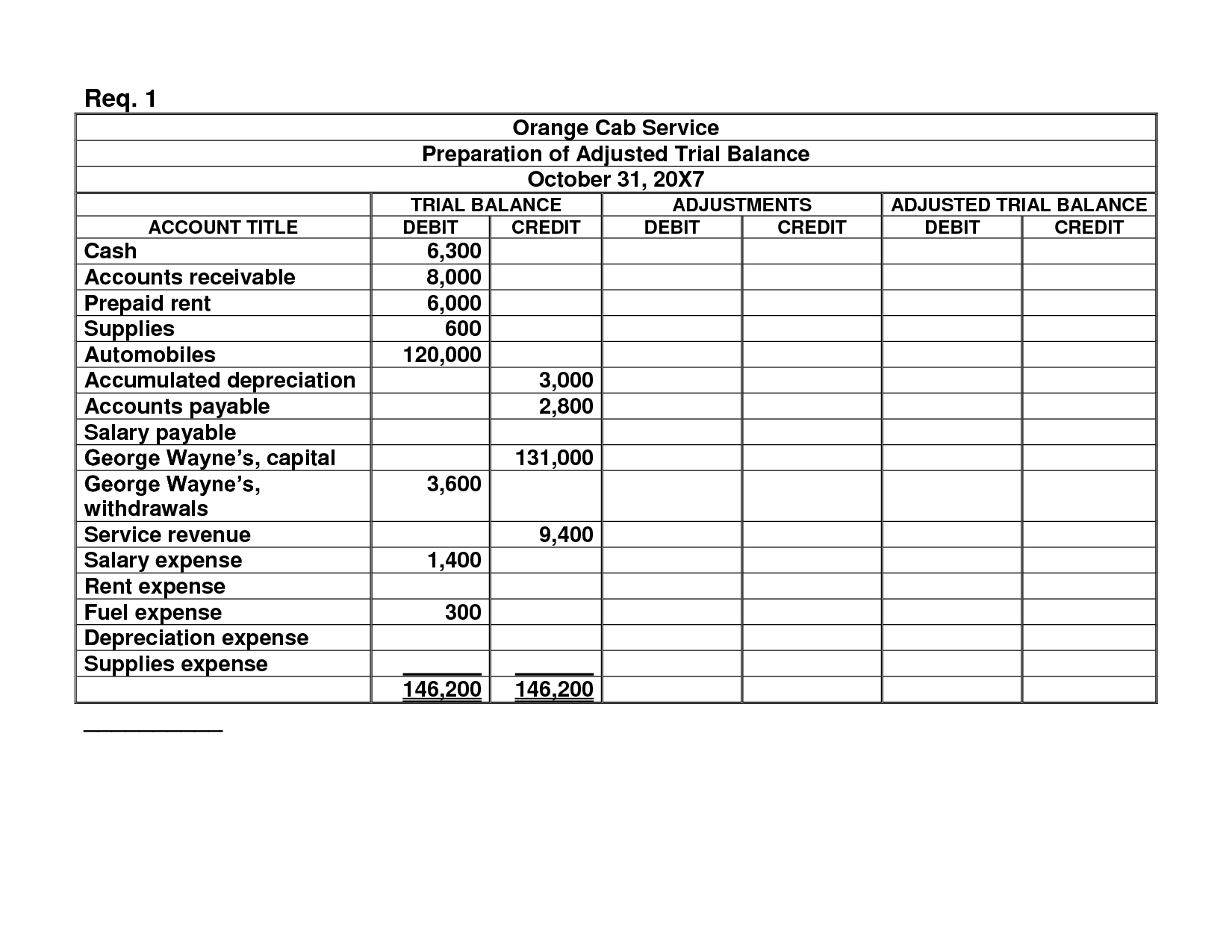

Before preparing the financial statements, an adjusted trial balance is prepared to make sure total debits still equal total credits after adjusting entries have been recorded and posted. As with the unadjusted trial balance, transferring information from T-accounts to the adjusted trial balance requires consideration of the final balance in each account. If the final balance in the ledger account (T-account) is a debit balance, you will record the total in the left column of the trial balance.

Financial Statements

Total expenses are subtracted from total revenues to get a net income of $4,665. If total expenses were more than total revenues, Printing Plus would have a net loss rather than a net income. This net income figure is used to prepare the statement of retained earnings. An income statement shows the organization’s financial performance for a given period of time.

Best Business Bank Account for Sole Proprietor: Top Picks for 2025

However, this time the ledger accounts are first updated and adjusted for the end-of-period adjusting entries, and then account balances are listed to prepare the adjusted trial balance. This method is time consuming but is considered more systematic. It is usually used by large companies where a lot of adjusting entries are prepared at the end of each accounting period.

- For example, IFRS-based financial statements are only required to report the current period of information and the information for the prior period.

- Under both IFRS and US GAAP, companies can report more than the minimum requirements.

- That is because they just started business this month and have no beginning retained earnings balance.

- Once all the accounts are posted, you have to check to see whether it is in balance.

The accounts that have been affected because of adjusting entries for the month of December are shown in red font in the adjusted trial balance. It is just for the purpose of explanation, and you don’t need to change the color of account titles in your homework assignments or examination questions. Note that only active accounts that will appear on the financial how to create a management report in xero statements must to be listed on the trial balance. If an account has a zero balance, there is no need to list it on the trial balance. There’s also a chance it’ll fail to flag entries incorrectly coded to the wrong accounts, which can ultimately lead to inaccurate financial statements. Inthese columns we record all asset, liability, and equityaccounts.

With an adjusted trial balance, necessary adjusting journal entries are incorporated in the trial balance. In the above example, unrecorded liability related to unpaid salaries and unrecorded revenue amount has been included in the adjusted trial balance. This trial balance is then used to prepare financial statements. Treat the income statement and balance sheet columns like a double-entry accounting system, where if you have a debit on the income statement side, you must have a credit equaling the same amount on the credit side. In this case we added a debit of $4,665 to the income statement column.

If the debit and credit columns equal each other, it means the expenses equal the revenues. This would happen if a company broke even, meaning the company did not make or lose any money. If there is a difference between the two numbers, that difference is the amount of net income, or net loss, the company has earned.

The statement ofretained earnings is prepared before the balance sheet because theending retained earnings amount is a required element of thebalance sheet. The following is the Statement of Retained Earningsfor Printing Plus. Once all ledger accounts and their balances are recorded, thedebit and credit columns on the adjusted trial balance are totaledto see if the figures in each column match. The final total in thedebit column must be the same dollar amount that is determined inthe final credit column. Once all ledger accounts and their balances are recorded, the debit and credit columns on the adjusted trial balance are totaled to see if the figures in each column match.

Those balances are then reported on respective financial statements. The 10-column worksheet is an all-in-one spreadsheet showing the transition of account information from the trial balance through the financial statements. Accountants use the 10-column worksheet to help calculate end-of-period adjustments.